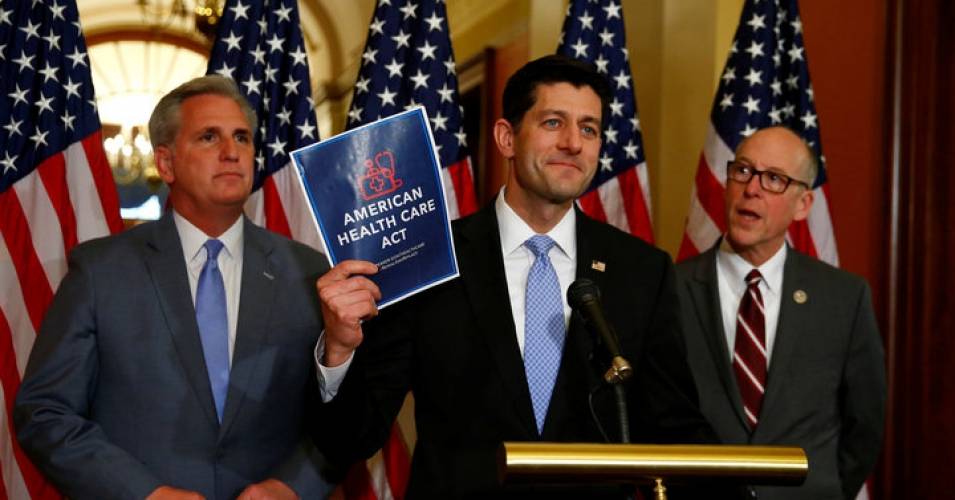

Last Monday, the GOP unveiled its bill to repeal and replace the Affordable Care Act known as the American Health Care Act (AHCA), aka Republicare. As of this writing the bill has passed the House Ways and Means committee and the House Energy and Commerce committee. It is expected to receive a full house vote before the next congressional recess in April. Things are moving quickly with this bill, so quickly that the Congressional Budget Office hadn’t yet scored it for potential costs or potential impact on the insured population before it was sent to committee, something they were able to do with the ACA. In fact, even though they’ve released their initial estimates there are still parts of the bill they haven’t had time to fully analyze.

However, that lack of information didn’t stop congressman Rodney Davis (R-Taylorville) from supporting the bill. A day after it was unveiled he released a statement fully supporting Republicare. His reason for doing so? Nobody seems to like it all that much.

One more time in case you missed it…. according to Congressman Davis, this bill is good because most people don’t seem to think it’s very good.

Rep. Davis was very specific in his labelling of those in opposition to the bill, taking special care to say, “when people on the far sides of both parties are unhappy, then you usually know you’re doing something right”, firmly placing himself in what he clearly believes is the sensible middle-ground. In a Facebook post he even went so far as to label those opposing it as the “extremes” of both parties. Glossing over the fact that assuming the truth lies between two extremes is a common logical fallacy, there’s absolutely 0 evidence that the groups opposing this bill are in any way, shape, or form extreme to begin with.

As of this writing, the most notable groups in opposition to this bill include; The AARP, The American Hospital Association, the Federation of American Hospitals, The American Medical Association, American Nurses Association, American College of Physicians, National Nurses United, National Physicians Alliance, and the Association of American Physicians and Surgeons. This collection of fringe radicals have all released statements opposing the bill.

Now if these organizations, all of whom represent the most experienced and knowledgeable people in the industry aren’t convincing enough, just take a look at the Congressional Budget Office’s analysis (I’ll go over this in depth in parts 2 and 3). 24 Million newly uninsured by 2020. Quality and affordability of coverage for the vast majority of Americans will decrease.

For Rep. Davis to continue to support this bill, despite the overwhelming opinion of healthcare experts, and a mountain of evidence indicating that it will likely result in less coverage, lower quality care, and higher costs, he must know something about it that we don’t. Considering he has never practiced medicine, has no experience working in healthcare, and had to have another congressman answer healthcare questions for him during his tele-town hall, the benefits of this bill must be painfully obvious to even the most casual observer. Being a casual observer, I decided to take a look at it myself. I figured the best place to start was with the “repeal” aspect of “repeal and replace”. That’s what I’ll be focusing on in Part 1 of this story. Part 2 will cover the “replace” aspect of Republicare, and Part 3 will cover my opinion/final thoughts on the bill as a whole, and the process by which it has come to be.

So, what parts of the ACA does Republicare get rid of? For starters the individual mandate is gone. This is one of the least popular aspects of the ACA, and has been a part of pretty much every potential GOP plan for the last 7 years. No longer will you be penalized for not having insurance. Also gone (starting in 2018) are the taxes placed on high-income individuals, medical devices, and high-salaried insurance executives (anyone earning over 500K/year), as well as the elimination of the famous “cadillac” tax. Finally, Republicare repeals a mandate within the ACA that all healthcare plans must have an actuarial value of at least 60% (don’t worry, this is a really obscure aspect of the ACA, I’ll explain in a minute). These are significant changes, and they will have a significant impact.

Now, obviously these aren’t the ONLY things being repealed (the mandate requiring employers to provide health insurance for their employees will be eliminated as well), but in my view these are the most significant changes, and will likely have the most impact. To start, we’ll look at the individual mandate, but before we look at what effect eliminating it will have, I want to (very) briefly discuss why it was a part of the ACA to begin with.

The individual mandate was the ACA’s way of pulling young healthy people into the market. This was accomplished by making those who could afford insurance but chose to go without pay a fee. The reasoning behind this was that by having a good mix of healthy/sick people in the individual market and pooling the risk, costs go down for everyone. This is pretty much insurance 101.

With the individual mandate gone, there is absolutely 0 incentive to have insurance if you’re young and/or healthy. Under Republicare, you can go without insurance for as long as you want with no penalty. When you do decide you need coverage, you just pick up insurance at a 30% markup for a year, get treated, and drop your insurance again. There is nothing in this plan to stop you from doing this. This will likely have a catastrophic effect on the individual market. If there is no incentive for healthy people to buy insurance, then the ONLY people in the market will be the people that actually need insurance, i.e., those that are currently sick, those with pre-existing conditions, the chronically ill, etc., etc. Unsurprisingly, sick people are incredibly expensive to insure, and as a result insurance companies will have to either make significant cuts to the plans they sell, raise premiums dramatically, or leave the market altogether. Ironically, rising premiums and lack of insurer choice are two of the main reasons Congressman Davis says the ACA needs to be repealed (although rising premiums may be an overstated crisis, and some insurers have left the market for extremely cynical reasons).

There’s also the not insignificant issue that a lack of a mandate brings about for those with pre-existing conditions. As I noted in a previous article, without a mandate the only real way to ensure those with a pre-existing conditions receive adequate and affordable coverage is for the government to pump 178 billion dollars per year into the market. The current iteration of Republicare only allots 100 billion over the next 10 years.

Now, the next major change under Republicare is the elimination of the ACA’s taxes. These taxes fell mostly on the wealthy, specifically: couples making more than 250K a year, taxes on investment income, and a provision that stopped insurance companies from deducting their employees salaries from their taxes if those employees made over 500K a year. Estimates put the loss in revenue over the next 10 years at 600 billion dollars. Put another way, this is a 600 billion dollar tax cut that will almost exclusively benefit the wealthiest 1-2% of Americans. More worrying than that however, is that this loss in revenue has no obvious offset in the current version of the GOP’s plan, meaning that the GOP haven’t explained how they’re going to be paying for it. This has caused many fiscal conservatives to abandon the plan entirely.

An important note here regarding taxes: the tax provisions within the ACA extended the life of Medicare by 10 years (something Congressman Davis lied about during his tele-town hall). In its current form Republicare would decrease the lifespan of Medicare by as many as 5 years.

Now, the final thing we’ll look at is the elimination of the “actuarial value” benchmark created by the ACA. Put simply, the ACA mandated that any “bronze” plan had to have an actuarial value of at least 60%, which meant that someone with that plan would be responsible for roughly 40% of their healthcare costs (paid for via deductibles, copays, etc.). Silver plans had an actuarial value of 70%, gold 80%, and platinum 90%. This was the ACA’s way of ensuring every plan covered at bare minimum 10 essential health benefits. Those were/are: ambulatory services, emergency services, hospitalization, maternity and newborn care, mental health services and addiction treatment, prescription drugs, rehabilitative services and devices, laboratory services, preventive services, wellness services, chronic disease treatment, and pediatric services.

Under Republicare, and without any sort of actuarial benchmark, insurance companies would be free to pay as little as they want for these benefits, and although the current iteration of this bill preserves the mandate within the ACA that out-of-pocket costs cannot exceed $6,000, outside of that insurance companies are mostly free to do as they please. This is an incredibly devious way for conservatives to get around the issue of covering these essential benefits by passing the responsibility (and the resulting blame) onto insurance companies. Making any cut to benefits such as maternal care or mental health treatment would be extremely unpopular in the public eye. So instead of making the cut themselves and taking the PR hit that would come with it, conservatives are repealing this obscure piece of legislation, something the vast majority of people will have never even heard about, let alone concern themselves with. In this way they believe they can have their cake and eat it too. They will receive praise for preserving these essential benefits, but behind the scenes will have created a situation in which people will likely pay significantly more for them.

Now that may sound like a slippery slope argument but make no mistake, insurance companies will very likely be forced to pay for a smaller portion of these services, as a matter of fact Republicare virtually guarantees it. As I mentioned earlier, with no incentive for healthy people to buy insurance, the market will be composed primarily of the most expensive people to insure. As a result, insurance companies will have to come up with other ways to control costs. It’s pretty easy to connect the dots here. If there’s no longer anything in place to make sure they pay for these benefits, they simply won’t pay for them when push comes to shove, and unless significant changes are made, it absolutely will.

Pay close attention to this maneuver in which conservatives attempt to reap the rewards of preserving these popular aspects of the ACA while simultaneously sabotaging them behind the scenes, as it will come up again in Parts 2 and 3 of this story.

By repealing these aspects of the ACA, Republicare has dug a concerningly deep hole for itself. Keep in mind, we’ve still yet to discuss how Republicare will restructure Medicaid (I’ll be looking at this in part 2) and the worrying implications of that change. The current iteration of this bill leaves the GOP with a plan that they likely can’t pay for without drastically decreasing the number of insured, or by making significant cuts to quality/affordability of care.

In Part 2 of this story we’ll dive into the “replace” portion of this bill and see if it’s up to the substantial task of delivering on the promise Congressman Davis and his colleagues made during the election to provide Americans with a superior alternative to the Affordable Care Act. As it stands, they’ve got a long way to go.